Four Models

Possible Real-life Meanings of - Random Variable

- Time to event

- Survival time after cancer diagnosis

- Time in remission

- Recovery time after surgery

- Dollar amount of an auto insurance claim

- Dollar payment on a medical malpractice policy in one year

- Number of claims submitted in six months

Cumulative Distribution Function (CDF)

Definition

The cumulative ditribution function is also called the distribution function. It is usually denotes as or , for a random variable . It represents the probability that is less than or equal to a given number. That is . The abbreviation cdf is often used.

Non-decreasing

Right-continuous

,

Survival Function

Definition

The survival function, usually denoted as or , for a random variable is the probability that is greater than a given number. That is,

Non-increasing

Right-continuous

,

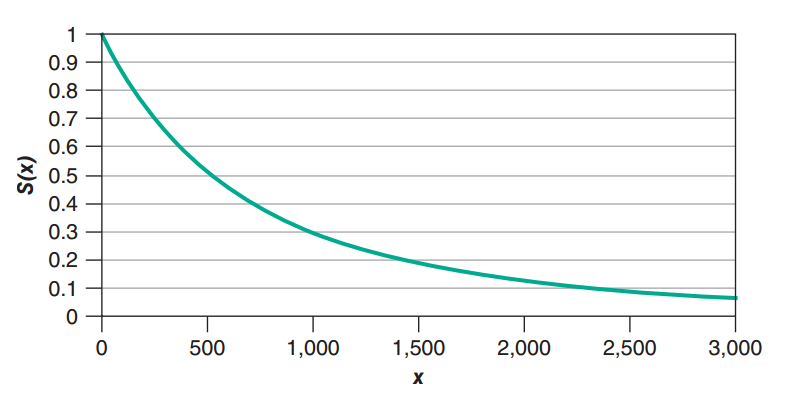

Exponential Survival Function

Probability Density Function (PDF)

if derivative exists

Hazard Function

Cumulative Hazard